")

Are you worried about paying for college as an agency owner? That’s a wise worry. Your kids likely won’t get financial aid, after schools consider your business pass-through profits and other factors. That means if they go, your family will pay full price.

It’s important to save for college. But many other decisions impact what you’ll pay. In this article, I’ll walk through some of those decisions and options—including finding the right path for their higher education goals.

Not everyone should start at a four-year school. Even when they do, their major and on-campus choices impact whether they’ll get a job in four years, need a fifth year, struggle to find a job, or drop out altogether.

My goal is to share points to consider during your decision process. The article series won’t help you make all the decisions—and you’ll want to consult with your financial planner and others. But getting the right answers starts by asking the right questions. In theory, at least: When you pay less, you won’t have to save as much.

Paying for college: 4-part series for agency owners

This article is Part 2 in a four-part series on preparing for—and paying for—college:

- [Part 1] How Much to Save for College, and Where to Start (e.g., elementary school or younger)

- [Part 2] How to Pay Less: Choosing the Right Path (e.g., your kids are in middle school) — this article

- [Part 3] Get More for Your Money: Raise Their College ROI (e.g., your kids are in high school or college already)

- [Part 4] Q&A with an Expert on Paying for College: Stephen Boatman, CFP®, CSLP® (with answers to 27 questions)

You can make the most of this “Part 2” article if your kids are in middle school (or early in high school). Why? Because they’re old enough to participate in the process, yet they still have time to explore.

My advice revolves around a core assumption: When you spend less on higher ed, you won’t need to save as much. For some students, that means an associate’s degree or a trade—and skipping a bachelor’s degree altogether. Or perhaps a different initial path—instead of immediately going to a 4-year school—to give them time to decide what they want. Consider the total investment: you pay less when they pick the right school—and graduate in four years instead of five years.

You benefit from helping your kids find the right path for them. Let’s consider nine points to help accomplish that goal.

9 points to consider: Save money by choosing the right path in higher ed

The “right” path is relative. It’s about the best path for your family—including your child—based on where you are today and where you realistically expect to be. Even when college is years away, consider what your AGI (Adjusted Gross Income) will be when they graduate.

- Recognize that you’re unlikely to receive financial aid. Because colleges count your salary and pass-through profits as income—and may even include the valuation of your agency as an asset—they see you as rich. You might not feel rich, but agency owners will likely pay full tuition for college. Fortunately, there are ways to save money—including alternate paths that might provide a higher total ROI.

- Define success. What’s your ideal outcome, your minimum-acceptable outcome, and your worst-case outcome? (More on that here.) This will be unique to your family, your child, and the current point in time. Their ideal path likely is different from your ideal path. Do they “need” the equivalent of a six-figure income to be happy? Success might include graduating debt-free, getting a first job in a career they’ll enjoy, or ending college with a stronger relationship with you than before.

- Identify paths to success. For many, it’s going immediately to a four-year school. For others, it’s starting at a community college—and potentially stopping with an associate’s degree, depending on their goals. And for others, working in a trade might be their key to success—and potentially becoming a business owner themselves someday, if they choose. It might also include building in time to figure out what they want—as a “gap year”—before they jump into a new formal education path. Do they want to become famous on social media? If you’d support them moving to New York or LA to pursue becoming an actor, you might likewise support them living at home for a year to try to make it as a social media influencer.

- Decide how your family will support them in their goals. This includes financial support for tuition, of course. But it also includes how you’ll approach their living expenses—for instance, if they choose to live at home, will they need to pay some rent? How might you adjust the “house rules” as they shift from “your child” to “your roommate”? What might you cover if they need to change plans—for instance, transfer to another school or add a year due to a major change? How much will they need to contribute to their education? If they choose a cheaper path today, would you commit to helping with graduate school, starting a business, or buying a house? If you’re not married to their other parent, some of this may require painful but important conversations. And when you have multiple children, consider that you’re setting a precedent—if you offer 100% coverage for your oldest, their younger sibling(s) will reasonably expect the same.

- Look at how you’ll pay for what you’re willing to commit. That impacts what options they can consider. This likely includes paying from college savings, paying cash for tuition as it comes up, possibly co-signing on a loan, and potentially helping pay down debt after they graduate. As of 2026, Harvard will cost ~$350K over four years. But even a flagship state school will cost an in-state student $150-180K. Private liberal arts colleges will be somewhere in between. If they start at a community college, their two-year program might cost $30-45K (depending on where they live). A trade apprenticeship program might have a training fee, but it also means the living expenses of working for several years to become a journeyman.

- Discuss boundaries around what your family will commit. Your child deserves to know what you’re willing to spend and what you expect from them. If they apply to an $80K/year school and get in, will you pay for them to attend? Or should they lower their sights or accept that they won’t attend the most expensive school? Consider the classic Krueger & Dale research, which found “that for students bright enough to win admission to a top school, later income ‘varied little, no matter which type of college they attended.’ In other words, the student, not the school, was responsible for the success.”

- Dig into ways to fulfill their ideal path. For example, this might include reviewing which in-state schools would meet their needs, identifying liberal arts schools that would fit their personality and goals, or doing informational interviews with people in a trade they’re considering.

- Consider ways to boost your ROI from the program. If you spend $200-300K on a school, your student’s choices can greatly impact the return on that investment. This includes school selection, major selection, and college-level extracurricular choices. I share more about this in Part 3.

- Execute the plan… and keep saving money. Your financial planner can advise you on the specifics. But the more you save, the better an outcome you’ll likely see. For instance, you can pay for the study abroad program, take on fewer loans, pay off the loans faster, or have money left over to help with post-graduation expenses.

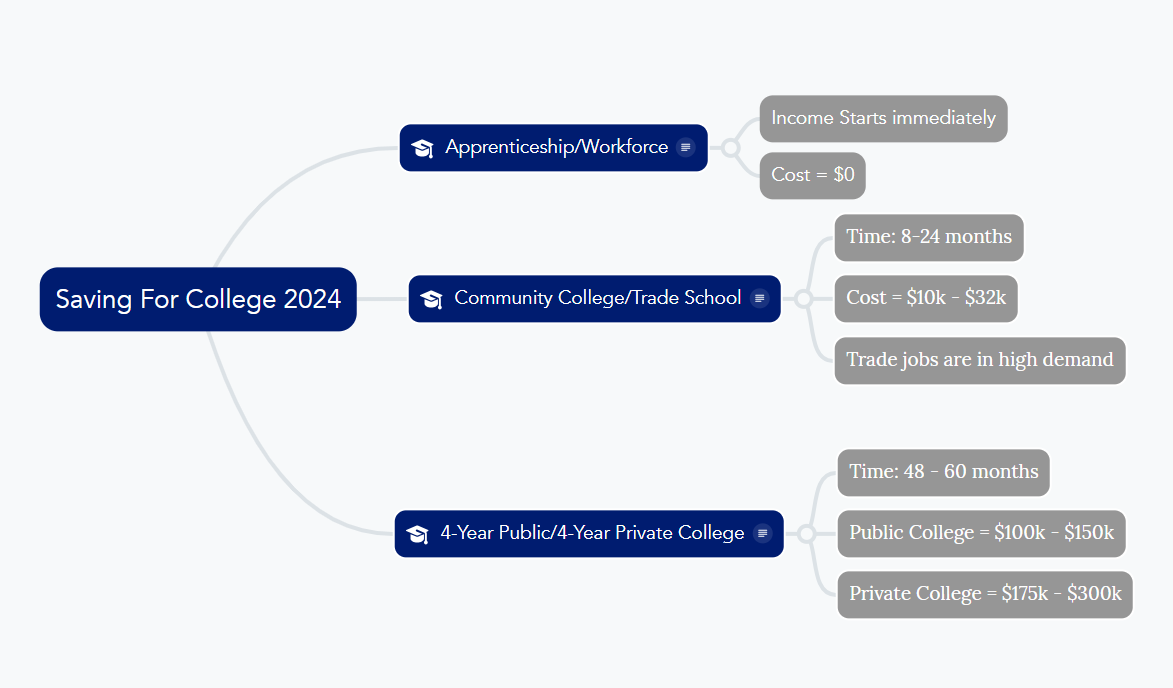

Stephen Boatman, our financial expert in Part 4, shared this chart (click the image to expand).

College pathways chart by Stephen Boatman, CFP, CSLP (click to see full-size image)

There are other ways to spend less, too—even if they still pursue getting a bachelor’s degree. Let’s consider some options.

21 more ways to pay less for college (directly or indirectly)

You pay less overall when your child graduates promptly—and “launches” to a self-supporting full-time job. With that in mind…

1. Enlist your child to do [most of] the legwork. It’s tempting to do all the research yourself—checking websites, running the calculators, filling out the forms, and calling people. But they’re an adult—or soon to be one. If they can’t—or won’t—share the workload, that could be a red flag about their college readiness. But now you can address it before they’re potentially hundreds or thousands of miles away.

2. Consider a “gap year,” especially if they’re not sure what they want to do. For instance, a year in a program like AmeriCorps might be the perspective they need. They may struggle to shift back to academic mode if they’re working in a less-structured role (e.g., a full-time minimum wage job). Or it might motivate them to get back to school. You probably don’t want to let them do “nothing”—for instance, living at home for a year without school, a job, or other responsibilities—unless mitigating circumstances exist.

3. Consider AP, IB, or dual-enrollment credits. Thanks to Advanced Placement (AP) classes, I started college with a semester’s worth of credits. Your child can do the same via International Baccalaureate (IB) and college dual-enrollment programs. This gives them the option to graduate early—saving you money—or flexibility in exploring majors. For instance, one of my siblings graduated from college in just three years. This won’t be a match for everyone, but it’s worth considering.

4. Merit scholarships “lurk” in unexpected places. Most won’t cover the entire cost of school, but they can make an impact—and help your student develop additional skills. And since you’re paying full price, the school isn’t going to reduce aid accordingly—the scholarships will save you real dollars. For instance, I won a public speaking competition that netted the equivalent of $4,000 today and got a similar amount as a credit union member.

5. Sports scholarships have promise… but come with many strings attached. Unless they’re going pro, weigh how sports commitments will impact their academic performance and post-college career. Getting a spot on the team doesn’t guarantee 100% funding, or even partial funding. And it doesn’t guarantee funding for a full four years, especially if they’re injured or otherwise lose their spot on the team. Be sure to enlist a lawyer to help you navigate the fine print. Also, a lower-ranked school may be willing to offer more money; if this means graduating debt-free, the academic “downgrade” might be worth it.

6. Self-motivated students can “punch above their weight.” When I was in college, top management consulting firms didn’t recruit on campus. So, I did my networking—including informational interviews with half a dozen alumni working at a well-regarded firm. I also snagged a first-round phone interview with McKinsey. However, as I tell business students when I do guest lectures, your college and first job are important—and “underemployment” is risky—but academic pedigree tends to become less important over time.

7. Depending on their career goals, graduate school rankings might be more critical than undergrad rankings. Consider the full picture. If they do well in college—for instance, taking the most rigorous classes at a lower-ranked (and less expensive) school—they could still get into a well-ranked graduate school. If their goal is to be a lawyer, doctor, or other professional, this might be worth it. But double-check with undergrad career services on graduate school “placements.”

8. How academic are your kids? If they won’t get into your state’s flagship school, what about other in-state schools? They might be more affordable, especially when you’re paying full price. Here in North Carolina, top-ranked UNC-Chapel Hill is $28K a year in-state (and $65K out-of-state). In contrast, other schools may charge less… including your choice of mountain or beach locations.

9. If your child is an average student, paying full price gives them options at lower-ranked schools. A close contact did recruiting at a small private liberal arts college. Their goal was to recruit a mix of students—but ideally, as many as possible who paid full price. This doesn’t directly save money… but if you’ll spend a lot anyway, consider the on-campus experience. I share more on “college ROI” in Part 3.

10. Talk with them about majors. I’m still working “in” my college major—but that’s somewhat unusual. It’s dangerous if they choose a school that requires them to pre-commit to majors their first year—it’s expensive to change later. This also applies in specialized programs, like in the arts. I met someone who studied acting—and every year, he had to re-audition to prove he was “worthy” to stay. He finally transferred elsewhere—but if he’d stayed, the atmosphere would have created an environment that encouraged a Sunk Cost fallacy. If you want them to take over your business (and they’re interested), consider if specific programs would be helpful in that process.

11. Consider schools that start with a “general education” core before requiring declaring a major. I liked that I didn’t have to declare my major until the end of my sophomore year. (There were some business prerequisites, but some counted toward my general ed or overall graduation requirements.) In contrast, some schools require committing in their first year. If they stick with the track, that’s fine. But if they need to “start over” when changing majors, you’ve added a fifth year—or more—in college expenses. Consider how you can support your child in choosing their “final” major as their first major. They can always do a major and a minor.

12. What are their career goals? If they want to become a teacher, they’re helping society… but society won’t pay them accordingly. That’s a strong case for going in-state. Other fields are more or less lucrative. In the New York Times, Ann Carrns notes: “The national average salary, four years after graduation, for [computer science majors] is about $105,000 … for electrical engineering, about $92,000.” But: “Does that mean you shouldn’t borrow anything if you want to major in, say, dance (with an average salary of about $30,000, four years out)? … If the earnings outlook for your major is modest, that’s an argument for being cautious with student loans.”

13. Consider a “community college first” strategy. Spending the first two years at a community college—especially if they live at home—will save money compared to the first and second years at a residential four-year school. If your child is an ambitious self-starter, this can work well. And STEM salaries with an associate’s degree are higher than you might think. If they plan to continue to a 4-year school, confirm if the community college has a “guaranteed acceptance” program for transfers.

14. Consider whether to hire an admissions consultant. You might hire someone to advise on applications, advise on choosing non-obvious schools, or something more in-depth. This could range from a few thousand dollars to a jaw-dropping $120,000 a year. (If you’re spending $120K on a college consultant, you don’t need this article series.) In the context of saving money overall—you’ll need to pay for their advice, but they might help your child find pathways to their goals.

“Advanced” options to save money

These aren’t for everyone, but they’re worth considering if they apply to your family.

15. Consider “front-loading” contributions to their 529. Stephen Boatman, our financial expert in Part 4, notes: “Most people aren’t aware that they can save up to $180,000 in a 529 account in one year.” You might not contribute that much up front (and you may not want to contribute that much). However, earlier contributions provide more time for potential market appreciation. The more the account grows, the less you need to contribute directly.

16. Consider free tuition options, like military service academies and public tuition forgiveness. But “free” is relative; a military commitment means time away from family, and the risk of death, injury, or PTSD. My parents were both career Army officers, but they noted it’s not for everyone. Civilian tuition forgiveness programs—for instance, working as a nurse for a non-profit hospital or as a teacher in a public school—require careful recordkeeping. Enlisting in the military could help them pay for school later, via G.I. Bill veterans benefits.

17. Consider moving to a state with better in-state schools, especially if you can downsize your house. Does your current state have strong in-state schools, or nearby states that offer in-state tuition to students from your state? In that case, you’re in good shape. But if you’ve been considering moving—perhaps toward your ideal retirement location—how are the public schools in your target state(s)? If your children are strong students, how about states that streamline college admission for top high school graduates? This is especially helpful if you can downsize to a less expensive house. But, of course, any move is disruptive.

18. Might their other parent get hired at a private university that offers tuition waivers for employee families? Search “tuition remission” as an employee benefit. For instance, the policy at Duke University covers up to two kids for up to eight semesters apiece—and it applies at any accredited university in the world. But there’s a “co-pay” involved, which means you’ll still need to save money. The policy at Boston University works on a sliding scale; it’s more generous (as a percentage) than Duke but limits coverage to tuition at BU itself.

19. Buy a rental property in their college town. If you are already investing in real estate, consider adding a property where your kids attend school. This gives them subsidized housing and gives you a new income stream (via their roommates or other tenants in a multi-family property). And if they’re responsible, you could pay them as the property manager. But I would only do this if you are enthusiastic about rental properties, and have the cash to cover the purchase and inevitable expenses. In college, I remember seeing a condo near campus that seemed like a good investment property. Sure enough, it’s now worth 50% more than inflation—plus the rental income it would have received over the past 20 years if my family had bought it.

20. Think carefully about “letting” them live at home. This saves money but carries a “failure to launch” risk. I’m glad I went to school a couple hours from home—it was easy to get home for break, but I had to solve my own problems while I was at school. Either way, discuss your expectations—do they need to work part-time to contribute to household expenses, or do you want them to focus 100% on school? What about contributing to household expenses and chores?

21. Talk to your tax advisor about advanced options. Are you on the cusp of the income cutoff, where your family would receive financial aid if your income were slightly lower? Stephen Boatman notes: “Deducting income by more than $200,000 in one year is possible for the right scenario through what’s known as a Cash Balance Plan.” And you may have other options, too.

What’s next? Helping them optimize their college experience

Paying “less” is relative; you’ll still spend a lot. But when your agency is more successful, you can afford to save more, which gives you options. Consider doing my Agency Value Audit, to get quick-win and big-win advice to help you reach your financial (and other) goals faster. Reach out here, and my team will recommend options.

Check out the rest of the series on paying for college (and read Part 1, too):

- [Part 3] Get More for Your Money: Raise Their College ROI (e.g., your kids are in high school or college already)

- [Part 4] Q&A with an Expert on Paying for College: Stephen Boatman, CFP®, CSLP® (with answers to 27 questions)

Don’t miss out—subscribe to my newsletter to get notified about future updates.

Question: From the list above, which tips will you explore?